How Does A Construction Mortgage Work?

Changes on Down Payment Rules

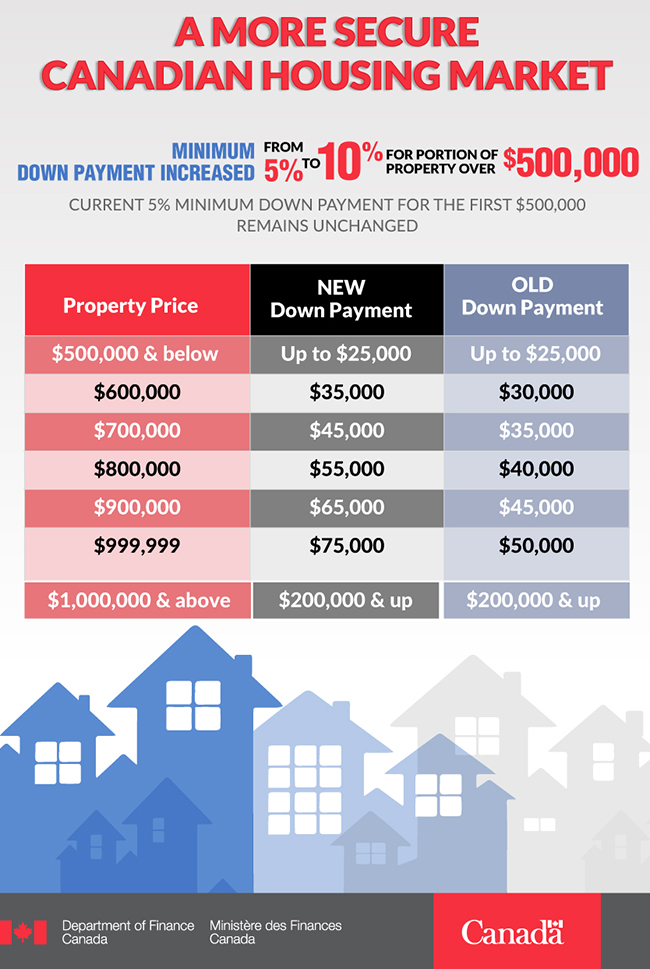

Just last Friday, the federal government announced significant changes to mortgage rules. The new regulations will increase the minimum down payment to buy a home that costs more than $500,000. The new plan will increase the minimum down payment from 5 per cent to 10 per cent for the portion of the home over $500,000.

Finance Minister Bill Morneau announced the changes to mortgage rules for homes over $500,000. Homeowners have to put down 10 percent on any portion of the price over $500,000.

At first glance people might think, ‘oh my goodness, I have to double the down payment’. That’s not the case. It is 10 percent for the additional amount over $500,000.

Let’s say you bought a $600,000 home in Vancouver. On the first $500,000 it is 5 per cent down. On the $100,000 taking it to $600,000, you have to have 10 per cent down. As a result, your down payment goes from 30,000 to 35,000.

A way to stabilize the market

So why do new home-owners have put down a larger amount on homes over $500,000?

The housing market has been very strong, but there has been a distortion in it. We’ve seen really high movement in Toronto as well as Vancouver. This new change is an effort to sort of slow things down.

Finance Minister Bill Morneau said the changes will help stabilize the housing market. It is a move to cool off the red-hot housing market in some large cities in this country.This change would slow down the real estate markets in Vancouver, Toronto, to name a couple, without slowing down the whole market.

Morneau stated that “by targeting higher priced properties, we’ll minimize the impact on many first-time home buyers about regional housing markets where activity is more moderate. While eliminating risk and tax payer exposure to the elevated housing markets in Vancouver and in Toronto”.

The Finance Minister said that the government doesn’t fear the market but they want to cool the market in some Canadian cities and create an environment that protects them. This decision comes just after the C.D. Howe Institute which came out with findings which apparently were taken into consideration for this decision that those who are first time home buyers are typically younger, have a lower income are very vulnerable. They don’t have emergency funds. What if they lose their job and what if rates start to go higher?

This is a way for the Finance Minister to say, ‘okay, we’re going to try to slow things down but we’re not going to bring the housing market to a screeching halt.’ To put some context around that, we’re talking about maybe in total 3.9% of new home buyers, 5% impacted in Toronto because it’s as hot as it is. 2.5% in Vancouver and surprisingly, because of the number of high risk mortgages, Calgary, Alberta is also going to be impacted. They don’t need any more things going on there to slow down their housing market. But what Bill Morneau is saying is that ‘these are mortgages that have to be insured by CMHC and we fund CMHC so were on the hook if people default’.

The new rules won’t impact current home owners

Existing homeowners will not be affected by the changes. They’ll go into effect as of February 15th of 2016.

You may be wondering if you’re a first time home buyer planning on purchasing in the New Year, are you going to feel punished by this or is this bad medicine for your own good? The new changes will definitely make them pause and question whether or not they are taking on too much.

A good thing that the Finance Minister pointed out was that he did not say it was effective immediately today. You have up until February 15th, 2016. It may cause new home buyers to reflect on whether or not they should be getting into this and if they are ready. The bottom line is that it is never necessarily a bad thing to have to put a little more money down because you end up paying less in interest and more money stays in your pocket in the long run.

Related posts