How Does A Construction Mortgage Work?

Getting A Bad Credit Mortgage

You made a few financial mistakes when life’s speed bumps got in the way, but now you’re on the right track and are ready to take the plunge into home ownership. The only issue is that you are not sure if your less than admirable credit history is going to keep a lender from giving you a mortgage loan. The good news is there are a few options available. The bad news is they aren’t always affordable. Here’s a guide to checking your credit score and, if you have no other option, get a bad credit mortgage.

STEP1. Checking Your Credit score

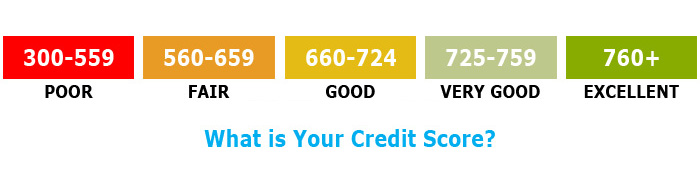

In Canada, your credit score is a number between 300 and 900 that is assigned to you by a credit bureau (in Canada, the two major credit bureaus are Equifax and TransUnion) and is used to give lenders an idea of how you have dealt with your credit in the past. To check your credit score, you can choose to pay Equifax or TransUnion for a report and your score, or you can choose to sit down with a mortgage broker and get them to check it for free. If you’ve been paying all of your bills on time, had no huge bankruptcies and generally don’t have more debt than you can afford to pay back reasonably, you should have a credit score above 680. If yours happens to be anything less, you’ll want to read on.

STEP 2. Finding a Bad Credit MortgageLender

If you have a credit score between 600 and 700 or above, you should have no problem getting a mortgage loan from one of the major banks, commonly referred to as “A lenders”. If, on the other hand, you have a credit score below 600, most Canadian major banks will not approve you for a mortgage loan. Instead, you’ll have to find a “B lender” or subprime lender. These financial institutions and trust companies work almost exclusively with people that have less than ideal credit scores. If you happen to have gone through a bankruptcy or consumer proposal within the last two years, you may even need to contact a private mortgage lender. If you are working with a mortgage broker, they should be able to recommend a lender they know will work with you.

STEP 3. SavingFor a Larger Down Payment

Lenders consider a number of things when considering your mortgage application, including your credit score, income and debt. If you have a good credit score, you can get a mortgage loan from most lenders with just a 5% down payment because you are seen as a low risk. If you have bad credit, the lender is taking on a higher risk by loaning you money, so most will want a much larger down payment, usually 20-25%. The plus side is that a larger down payment may give you a little more leverage when it comes to negotiating a fair mortgage rate because you are less of a risk than someone who has little equity in their home.

STEP 4. Preparing to Pay Extra Fees

You now know that you will have to save a larger down payment. You’ll also need to have a cushion set aside for additional fees. Lenders can charge up to 1% of the mortgage loan value for processing a bad credit application. Because banks don’t usually compensate brokers for bringing them clients with credit issues, your broker may also charge you an additional 1%. Keep these additional fees in mind and have that extra cash ready.

STEP 5. Dismissing Best Mortgage Rates

Your credit score has a direct impact on the lender you are eligible to work with, as well as the mortgage rate available to you. If you have good credit, you can work with the bigger banks and access the best mortgage rates. If you have less than ideal credit, you’ll have to work with a “B lender” or private lender and be subject to higher interest rates. Remember, your lender looks at your credit score and report to determine how much of a risk it would be to lend you money. If you want to be access a lower mortgage rate at your time of renewal, make all of your monthly mortgage payments on time and do everything possible to boost your credit score, including using a credit card responsibly and paying off any other debts.

Related posts