It’s Not Just Politics… Other Expenses Keeping Canadians Away From Spending on Housing

Variable Rate Mortgages: What Are The Pros And Cons?

Last week’s article covered some latest news about the Bank of Canada’s decision to increase the interest rate for mortgages and how it may affect homebuyers. One of the short interviews that was included in the text briefly discussed the difference between fixed rate and variable rate mortgage, but now, you can read more extensively about the variable rate mortgage, and what’s good (and not) about it.

A variable rate mortgage will change irregularly throughout the mortgage term. While your regular payment will stay the same, market conditions will dictate the interest rate. Unfortunately, this would impact the ‘amount of principal’ you pay off each month. When the rates on variable interest mortgages decrease, more of your regular payment is applied to your principal. Additionally if rates increase, more of your payment will go toward the interest. The amount of principal can be defined as both the payment on the initial size of a loan, and the amount still owed on a loan.

Variable rates are linked to the lender’s rate, which is determined directly on the Bank of Canada rate. Remember, the Bank of Canada is not a commercial bank and doesn’t provide services to the public. Instead, their main role, as defined in the Bank of Canada Act, is “to promote the economic and financial welfare of Canada.”

A variable rate mortgage typically offers more flexible terms than a fixed rate mortgage. They can be a cheaper than fixed-rate mortgages in the cost to break your loan before the term is up. People who demand the flexibility to exit a mortgage early at no cost can choose an open mortgage, but the cost is an extra-high mortgage rate.

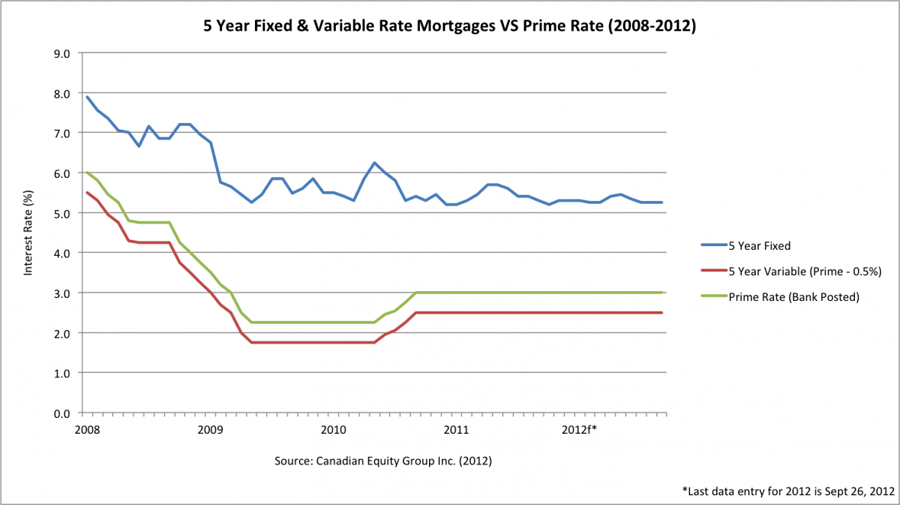

Right now, the current spread of more than a full % point between variable and fixed rates is the widest it’s been in Canada since 2011. James Laid, a mortgage expert, said “Whenever that happens, you do see a shift where consumers are more likely to see the increased risk of the variable being worth the savings that can be had immediately.”

He added that there’s ample evidence to suggest that both fixed and variables will be headed higher eventually. But he noted that it will take four rate hikes from the Bank of Canada to move the variable rate up to where fixed rates currently are. “And you would have to move past that to be in worse shape for the latter part of the loan,” he finished.

Mortgages get broken because either couples divorce, are swamped by debt and need to refinance, want to pay off their loan early, or they’re selling and moving somewhere else. Life circumstances can get complicated, so brokers and lenders must be more flexible. While potentially more expensive, a variable mortgage is like an insurance policy against upheaval or change in your life. If you needed to sell for some reason, you know that your penalty will be equivalent to three months of interest.

What are the disadvantages of choosing a variable-rate mortgage? If interest rates rates drop significantly, the borrower still continues to pay the higher rate. Also, even though you would be making smaller payments in the short term, there is a risk that the rate could go well up down the line, meaning bigger payments.

Another important aspect of a variable rate mortgage is the ‘5 year plan’. This plan fluctuates with short-term interest rates and is known to help borrowers save money over time. They come in two forms: open and closed.

A closed 5-year variable binds you to the terms of your mortgage for a duration of 5 years.

An open term gives you the flexibility to move to a fixed rate at any time, but interest rates are usually higher.

How do you calculate payments for a variable mortgage rate? There are two ways!

- Pay a set amount every month: the proportion of interest you pay changes based on the interest rate at the time. You can take advantage of today’s falling rate environment and pay down more of your principal while maintaining a constant payment.

- Pay a certain amount of principal and interest: the amount you pay each month moves up or down as interest rates change.

Thank you so much for reading! If you’d like even more information, you can contact us here. Have a great week!

Related posts