How Does A Construction Mortgage Work?

Canadian Mortgage Debt Has Never Seen Such Explosive Growth – $1.7 Trillion

Home sales might be slowing, but Canadians have begun one of the most epic debt binges ever. Bank of Canada (BoC) data shows outstanding residential mortgage credit reached a new record in June. It didn’t just “soar” to that level though. It showed explosive growth, like someone strapped a rocket to it.

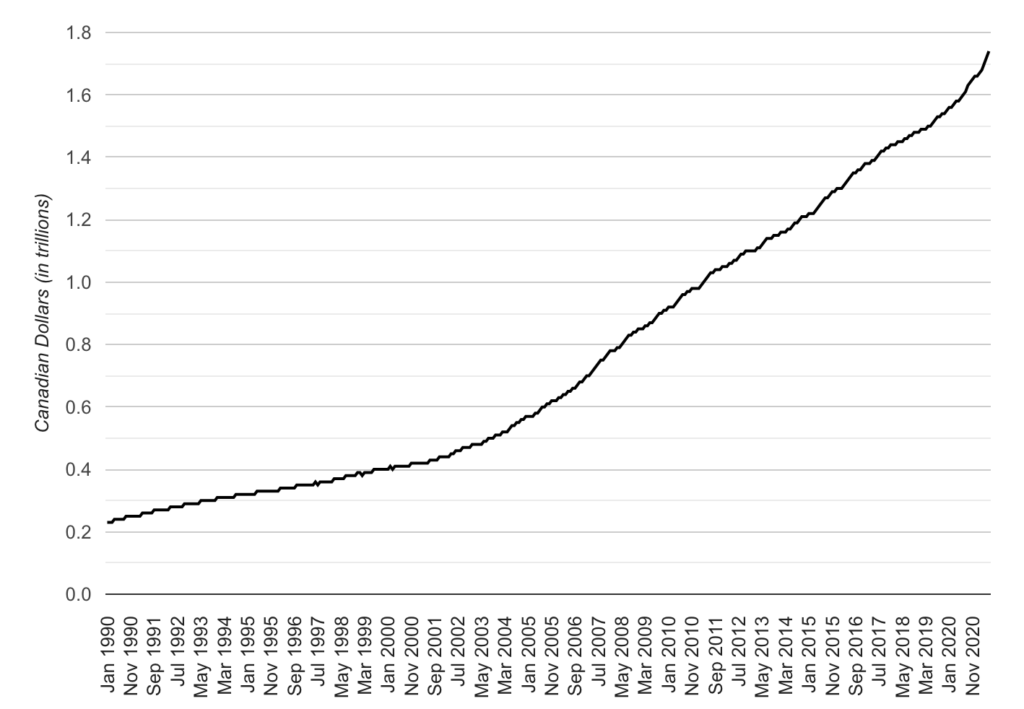

Canadian mortgage credit has been soaring the past few months — but nothing like we’ve just seen. The outstanding balance reached $1.7 trillion in June, up 1.37% ($23.6 billion) from a month before. Compared to a year before, this represents an increase of 9.21% ($146.7 billion). Those simple numbers have a whole lot to unpack this month, but we’ll try to stick to the key takeaways.

Canadian Residential Mortgage Debt

Source: BoC; Better Dwelling.

Canadian mortgage debt has never made a monthly jump like this. Let’s start with the monthly growth, which you know, is huge — but a percentage rate diminishes how big it is. When we say $23.6 billion, it’s a little different. It was the largest monthly dollar increase ever. There was never a point in Canadian history where this much was borrowed for residential mortgages. Over the past year, over one in seven dollars added to mortgage debt, was added this past June.

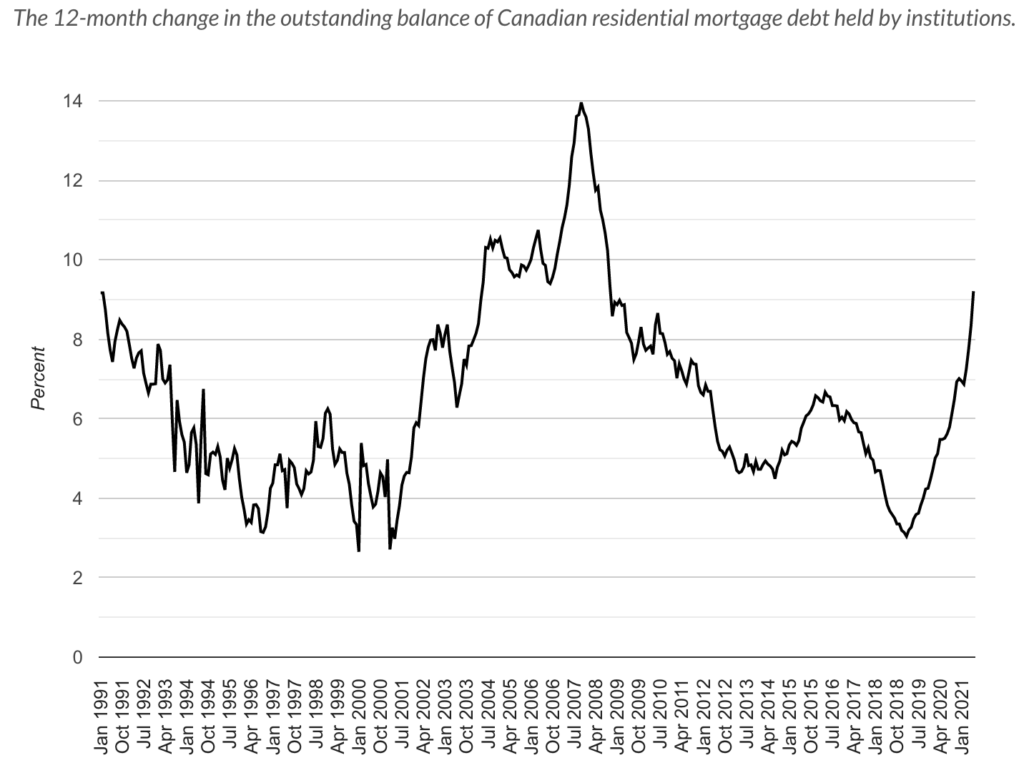

Canadians Add More Than The GDP Of Kuwait To Their Mortgage Debt

The debt added over the past year is also a mindblowing amount. The annual rate of 9.21% is the biggest number recorded since 2008. As for the dollar amount, it’s more than half the size of Alberta’s gross domestic product (GDP). Heck, the amount of dollars Canadians added to their mortgage balance is bigger than the GDP of Kuwait or Morocco. Not the amount spent, but just the amount added… just at institutional lenders. To say it’s a mindblowing waste of resources doesn’t quite capture it.

Canadian Residential Mortgage Debt

Source: BoC; Better Dwelling.

There are some important nuances to this data before coming to a conclusion. Statistics Canada (Stat Can) said, “There is normally a time lag between the sale of a home and the actual receipt of mortgage funds; however, borrowers may also be in the market for a new home, or otherwise be taking additional equity out of their home or consolidating debt when refinancing their existing mortgages.”

Essentially, this means homebuyers report more debt than would actually settle. As they receive mortgage funds for the home they sold, the balance would fall. While this may sound like Stat Can used this to dismiss concerns about the increase, it doesn’t really. This wasn’t the only month where that occurred. Since home sales have been sliding, that trend should have lowered the amount of mortgage debt, not necessarily increased it.

Mortgage Debt Surged As Borrowers Try To Beat The Stress Test

This more likely has to do with the mortgage stress test, which went into effect on the 1st of June. Uninsured mortgage borrowers often get pre-approved for their mortgage prior to the change in rules. This allows them to shop for homes after the date, but squeezes more buyers into a small window.

These typically only last for 90 days, so anyone who wanted a mortgage this year but didn’t want reduced buying, needs to buy in this small period. This also would provide a little context to the abrupt increase of home sales in July, despite flat prices. Buyers in a low inventory environment would normally have pressure to spend more. The market is now flooded with a type of buyer pushing their debt to the maximum.

One other reason pushing this number higher is refinancing. Equity withdrawals have always been popular, but with mortgages at negative rates in real terms — more people are likely withdrawing equity. This was a concern back in 2018 that regulators had expressed, but it’s 2021 so we’re pretending none of these issues existed prior. It cooled after that, but has been making a roaring comeback over the past few months. We’ll break those numbers down later this week.

Related posts