How Does A Construction Mortgage Work?

Fixed Rates Have Become More Desired by Canadians Once Again

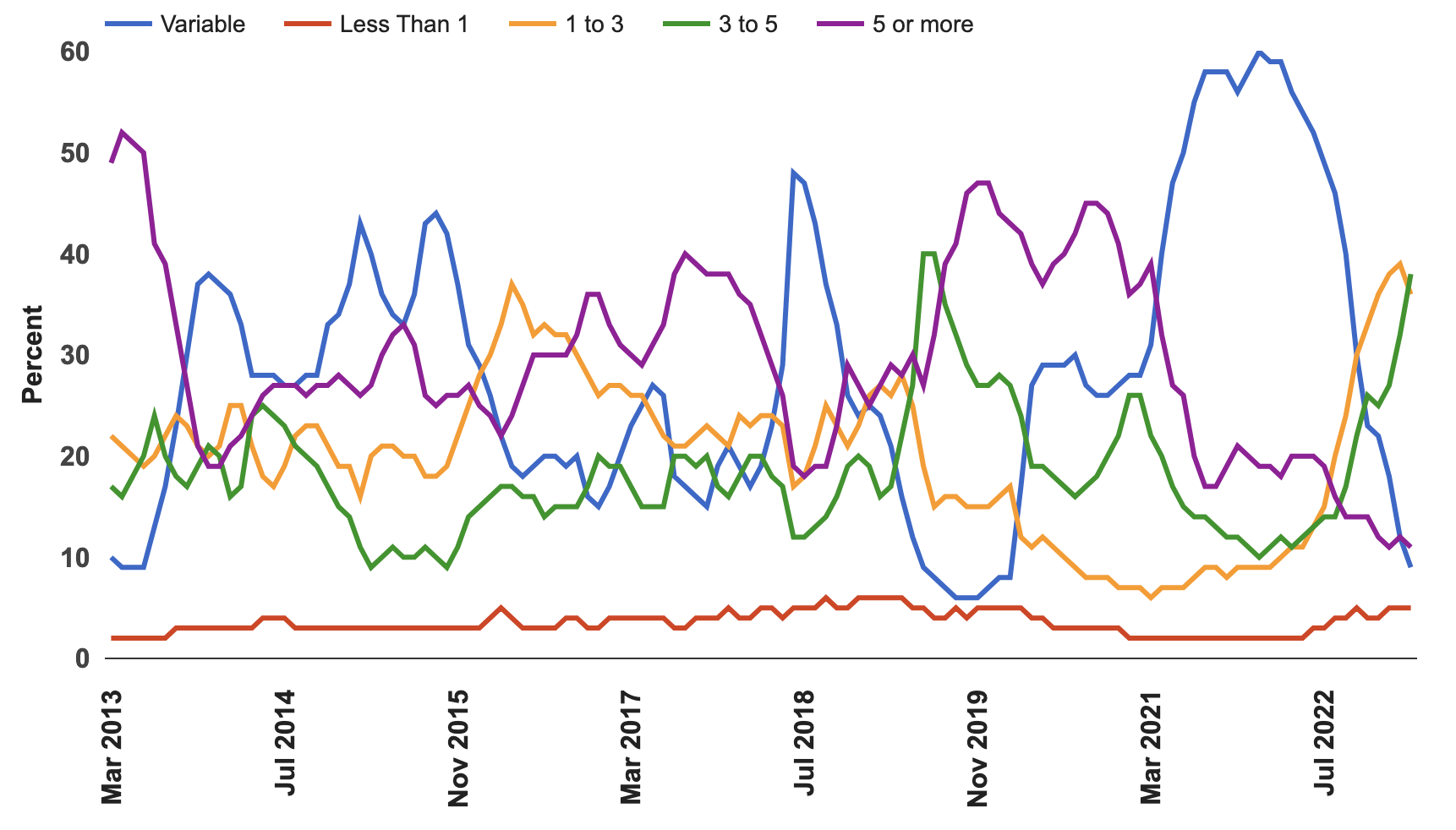

Canadian mortgage borrowers are fleeing unpredictable variable rates, and getting more leverage. Bank of Canada data reveals that nearly three-quarters of mortgages issued in March had rates fixed for 1 to 5 years. It’s a big change from a year ago, when most borrowers were opting for variable rates. Borrowers shifted their preferences after rates began to climb, grabbing cheaper debt—that also happens to be providing more leverage.

Canadian Mortgage Borrowers Are Seeking 1 To 5 Year Fixed Rates

Canadian homeowners are seeking out medium-term fixed rate mortgages. The largest share of new loans in March had 3 to 5 year fixed terms (38%), triple the share last year. It was followed by 1 to 3 year mortgages (36%), significantly higher than the 10% last year.

Canadian Mortgage Borrowers Are Opting For Shorter Fixed Rates

Source: Bank of Canada; Better Dwelling.

Part of the appeal is likely the significantly lower interest cost. New loans with 3 to 5 year fixed rates had an average interest rate of 5.15% in March, observing only a slight change from the January peak (-0.03 points). A 1 to 5 year fixed rate mortgage was slightly more expensive, averaging 5.54%, barely moving over the period (-0.01 points). Not much movement, but those rates are a lot cheaper than variable loans.

Variable Mortgage Rates Are Back To A Single-Digit Market Share

Most loans made last year had variable interest rates, but that changed fast. The share fell to just 9% of uninsured mortgage debt issued in March, down from 59% last year. It’s not too hard to see why—the average loan had an interest cost of 6.66% in March, up from 1.81% last year. New borrowers would be paying significantly more than shorter term loans, 1 to 5 years long.

Existing borrowers have also seen their costs surge, providing many warning stories.

Longer-Term Mortgages Aren’t Attractive To Borrowers Either

Fewer borrowers are seeking out long-term mortgage rates, despite stable costs. The share of mortgages with fixed rates for 5 or more years, fell from 18% last year to just 11% in March. The average rate (5.1%) is also much lower than variable mortgages, but didn’t have as much appeal as shorter-terms. It appears few are confident in the economy’s ability to carry higher rates.

The gap between variable and fixed rates doesn’t just mean a discount when opting for a fixed rate. It also provides more leverage, with home prices recently climbing lockstep with leverage. Any additional debt service capacity is being absorbed by the market.

The BoC recently voiced a concern over household indebtedness becoming a threat to the economy. At the same time, borrowers are seeking longer repayment terms, increasing vulnerability to households and the economy.

Related posts