How Does A Construction Mortgage Work?

From Debt Into Mortgage?

Consumer debt in Canada has reached $20,739 per person, on average.

Credit card spending and balances in Canada are trending upwards compared to recent years and more concerning, there’s an uptick in credit card accounts with missed payments.

If you’re a homeowner, you might be wondering whether you can use the equity in your home to reduce your payments, or the interest you’re paying on your high interest debt.

The good news is that you can – and there are a few ways to do it.

Read on to learn how you can consolidate your debt into your mortgage below.

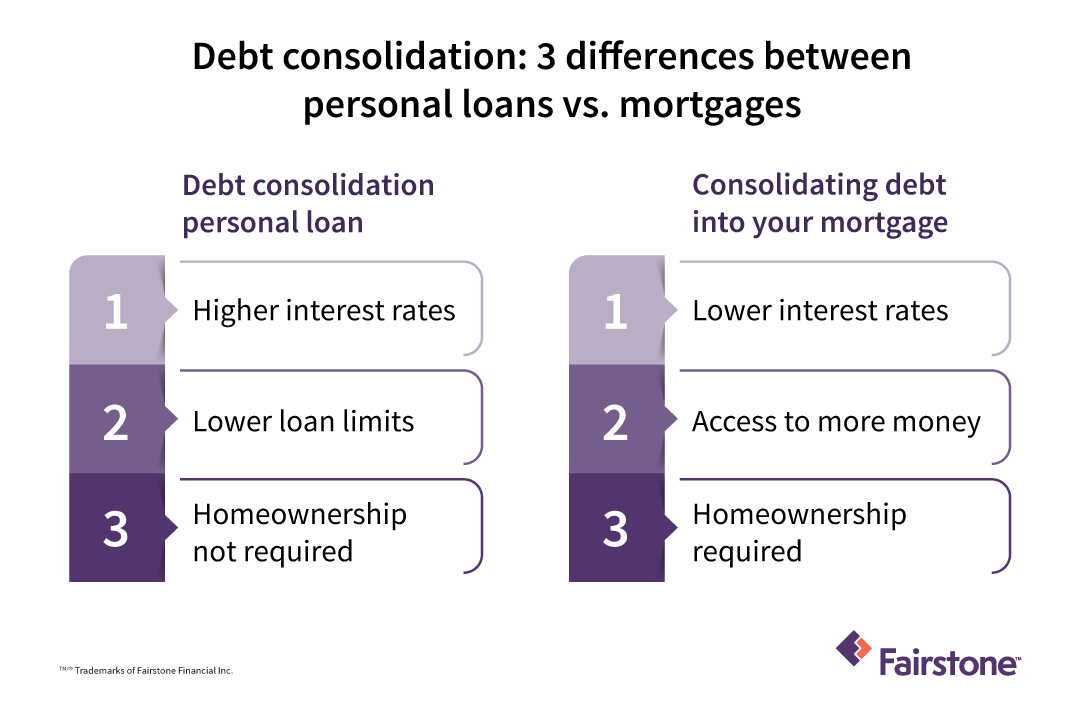

Debt consolidation loans vs. debt consolidation mortgage

The idea behind consolidating your debt is to take your high interest debt (typically multiple balances) and pay it off using one loan with a lower interest rate.

A debt consolidation personal loan is like a regular loan, but the money from this loan is used to pay off existing debts.

However, if you’re a homeowner, in addition to debt consolidation loans, you may have the option to consolidate your debt into your mortgage.

So, what are the benefits of a debt consolidation mortgage vs. personal loan?

Usually, consolidating debt into your mortgage means you will have access to a lower interest rate and a higher borrowing amount – and there’s other benefits to using your home equity to maximize your borrowing power – which we cover below.

3 benefits to consolidating debt into mortgage

Depending on how you set up your loan, using your mortgage to consolidate your debt can have a few benefits:

- A lower interest rate can mean less interest paid overall

- Depending on the payback period, your payments can be less – even if the interest rate is higher

- You will be left with one bill to pay, which can be simpler, easier to stick to and provide a clear date for when your debt will be paid

If you’re a homeowner, you may be able to tap into the equity you’ve built in your home to consolidate debt.

In order to consolidate your debt into your mortgage, you’ll need to have some equity in your home – which is the difference between what your home is worth and what you owe. You’ll also need to qualify for the loan or new mortgage.

How much equity you need and what you’ll need to qualify depends on which option you choose for debt consolidation.

How to consolidate debt into your mortgage

There are four main ways you can use your mortgage to consolidate your debt:

- Home equity loans

- Home equity lines of credit (HELOC)

- Refinancing your mortgage

- Reverse mortgages

Each one has different pros and cons and requirements to qualify, and we’ve included a helpful table at the end of this section to figure out which one might be right for you.

Home equity loans

Home equity loans use your home equity as collateral, allowing you to take advantage of benefits like higher loan amounts, lower interest rates and longer terms and/or amortization periods.

A secured personal loan and a second mortgage are both considered home equity loans because they are secured against the equity in your home.

One of the major draws for home equity loans is they don’t impact your first mortgage, meaning if your first mortgage interest rate is favourable, you can keep it as is and there are no fees for breaking your first mortgage early. Additionally, some people like the fact that the money they’re borrowing to consolidate debt is kept separate from the first mortgage.

A drawback to home equity loans is that their interest rates are usually a bit higher than a first mortgage.

Also, unlike a home equity line of credit (HELOC), once the money is paid back, it cannot be accessed again. This could be a benefit to some (who want to pay down debt and be done with it), but an inconvenience to others who like the idea of having the money accessible if they need it again.

Home equity line of credit

When you get a home equity line of credit, the lender gives you a limit you can borrow up to (limited to 65% of the value of your home, but the combination of your HELOC and mortgage can’t exceed 80% of the value of your home) and you borrow or repay money as you need to.

The main advantage of home equity lines of credit is you are only borrowing money as you need it – this can make HELOCs a good option for emergency funds.

However, HELOCs come with a few disadvantages:

- They typically have variable interest rates which means if interest rates go up, your payments will increase and could become unaffordable.

- HELOCs are revolving credit so if you have trouble managing your spending, you can end up with a large balance and can quickly get into trouble being able to pay it back.

Refinancing your mortgage

Refinancing your primary mortgage can be a powerful way to consolidate your debt because you can access lower interest rates compared to secured personal loans, second mortgages and lines of credit.

Refinancing your mortgage involves changing the terms of your primary mortgage. When you refinance your mortgage you can change a number of things about it:

- The amount you borrow – if equity is available, you could borrow more money than your current mortgage to free up funds for debt consolidation

- The interest rate (if a lower one is available) – lowering your payments and borrowing costs

- The payback period of the mortgage (the amortization period) – the longer it is, the lower your payments (and vice versa)

- The term – the amount of time you’re committed to the conditions of your mortgage with a specific lender

Depending on when you refinance your mortgage, and your mortgage terms, there can either be small costs or very large penalties to refinance.

In most cases, if you want to refinance your mortgage before the term is ending, your lender will charge you a prepayment penalty to break your mortgage. This is typically either three months’ worth of interest payments, or a complex formula called an interest rate differential. Depending on your interest rates and how much you owe – these penalties can sometimes be very expensive.

However, if you refinance your mortgage in between terms, you can typically avoid these penalties. You may still have costs associated with establishing a new mortgage, such as appraisal fees, title search and insurance, legal fees and registering the mortgage.

Reverse mortgages

Reverse mortgages are a loan product that’s gaining popularity in Canada. These are special loans available to homeowners who are 55 years or older.

If you are 55 years of age or older, and you own your home, you could borrow up to 55% of the value of your home through a reverse mortgage and use this loan to consolidate your higher interest debt.

Reverse mortgages have a few special features that make them attractive to borrowers. For example, you don’t have to make any regular payments with reverse mortgages.

While you’re free to make any repayments at any time during the loan, typically the loan is paid off when the last person on the title of the house dies, leaves or sells the house. At that time, the amount of the loan and interest is deducted from the money the seller would have received.

Reverse mortgages are also very easy to qualify for compared to the other consolidation options discussed here. This is because you already own the home and won’t be making any payments, so typically only an appraisal of the house value is required.

There are a few drawbacks to reverse mortgages you should be aware of:

- The fees can feel hidden to the borrower since they don’t pay anything until they sell the house or die

- The house has to be kept in a good state of repair, or the borrower could default on the loan

- There may not be any equity left to help pay for the next stage of retirement, or to pass on to your loved ones

- Interest rates can be higher than for traditional mortgages

- If you live in cooperative housing, you may not be eligible for a reverse mortgage

What is the best option for consolidating your debt into your mortgage?

Each of the four ways to consolidate your high-interest debt into a lower interest mortgage have pros and cons.

Because your mortgage is typically the largest debt and asset you’ll ever have – it can be tough to decide which option is best for you.

Consolidating your debt into your mortgage could potentially save you lots of money on your debt and simplify your bills, but there are drawbacks to be aware of too:

- If you have trouble controlling your spending, consolidating your debt will not solve the underlying problem. You may need to look into ways to get your bills under control and stop living paycheque to paycheque.

- Because you’ll be clearing off the balances on your credit cards or other high interest accounts, you might find it hard to avoid running up those balances again.

- You might end up with a higher interest rate than you have now depending on what you qualify for. While you might still be able to reduce the payments to a manageable level – you could end up paying more in the long run.

So, should you consolidate your debt into your mortgage?

When it comes to the question of whether debt consolidation is the right choice, there is no single answer – it depends on your situation, needs and your spending habits.

Debt consolidation can be a responsible option if you’re looking to consolidate repayments into one loan and find a lower interest rate. Using your mortgage to consolidate your debt can give you access to lower interest rates and longer payback periods, creating a debt consolidation plan that fits your budget.

However, there are pros and cons to using your mortgage for debt consolidation and each option offers different strengths and drawbacks.

Whether it’s the right choice for you and which method to choose depends on your situation and what your lender recommends.

Related posts