It’s Not Just Politics… Other Expenses Keeping Canadians Away From Spending on Housing

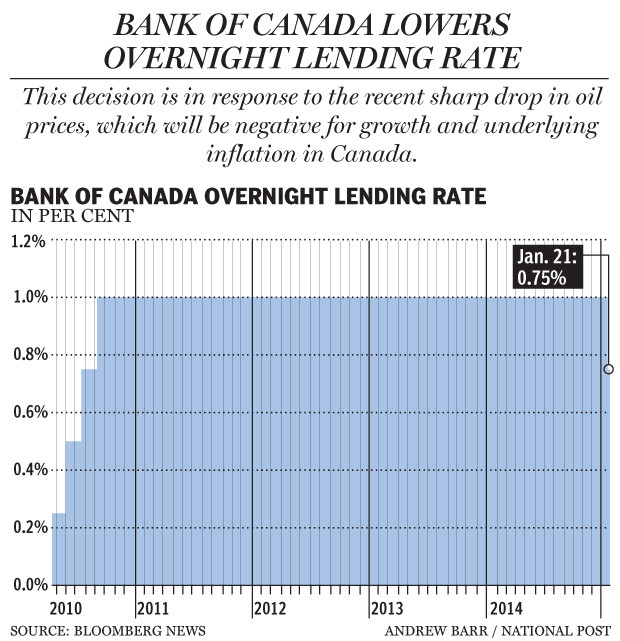

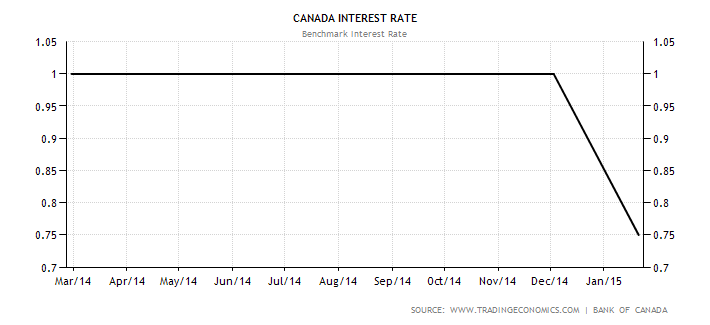

The Bank of Canada reduced the lending to 0.75 percent

The Bank of Canada is the first central bank in the Group of Seven to slash interest rates in response to plunging oil prices, saying the shock will contribute to inflation and business spending. The Bank of Canada shocked economy experts and financial markets on Wednesday January 21st by cutting its benchmark overnight interest rate by one-quarter of a percentage point, to 0.75 per cent. The rate, which influences lending rates across the Canadian economy, had stayed at 1% since September 2010, and was last cut in April 2009. Economy watchers did not expect this rate to change. This aggressive and sudden move says a lot about where the Bank of Canada sees the economy and inflation going.

Bank of Canada Governor Stephen Poloz said that the decision was made in response to the sharp drop in oil prices. “We generally prefer that markets not be surprised by what we do,” said Poloz. “In that respect, we took comfort from the observation that the consequences of the drop in oil prices appear to be well understood, and that the possibility of a rate cut had begun to enter markets in the last couple of weeks. Moreover, given the magnitude of the shock, we concluded that the benefits of acting now rather than waiting would outweigh the costs of any short-term market volatility that might arise.”

More borrowing ahead

Poloz called the drop “unambiguously negative” for the economy as it is insurance against potentially destructive effects such as weak inflation and a real-estate turndown. The oil shock has already led to layoffs and spending cuts in the oil and gas industry, postponed energy projects and a possible housing burst in Alberta. The entire country has been made poorer because Canada will generate less wealth from the oil it sells to the world.

The surprise move is not quite the direction that financial experts want rates to be headed as our society faces record household debt loads. Basically, this big cut in interest rates will encourage more borrowing. A rate cut such as this means big financial institutions and lenders are likely to lower their own interest rates for borrowers, encouraging Canadian consumers and businesses to take on more credit. The surprise is that this rate cut was made just as Canadian households carry record-high debt, the biggest domestic risk to the economy. However, the risks for the national economy and unemployment created by the oil shock greatly outweigh consumer debt, according to the Bank of Canada. Jobs will be harder to find and the economy will slow as the oil price crash bites in upcoming months. Poloz stated that the Canadian economy had been showing signs of growth before oil prices dived.

What this means for your mortgage

Canadian homeowners have basically gained a reprieve from an expected increase in mortgage rates this year. They are off the hook. The Bank of Canada uses the key rate to influence the borrowing costs commercial banks charge businesses and consumers, allowing the central bank to boost economic growth if there is a threat of a sharp downturn. The outcome of this drop will likely mean lower mortgage costs for homebuyers and a longer grace period, most likely till at least next year, before mortgage holders are pressed when the Bank of Canada begins to increase borrowing costs to head off a burst of inflation. The decreased mortgage rates are likely to boost sales and increase prices of homes in Central Canada, especially in Toronto’s hot property market where prices could climb as high as five per cent this year.

This news certainly will not discourage anyone from taking on more debt. The lower interest rates may encourage already quite heavily indebted Canadians to borrow even more, resulting in price inflation in home prices in cities like Toronto and Vancouver. This may get a lot of first time homebuyers into big financial trouble when the time comes. Fixed-rate mortgages are also likely to see a decline, as they follow bond yields, which will move lower due to the rate cut.

The bank also hinted at a possible spread of a real estate slump, like the one under way in Alberta, to other parts of the country. “The extent to which the downturn already evident in Alberta will spill over into other regions remains to be seen,” the bank pointed out in its monetary policy report.

Related posts