It’s Not Just Politics… Other Expenses Keeping Canadians Away From Spending on Housing

Do We Want The CMHC’s Help With Our Future Homes?

New week, almost new month, and it’s already springtime! January may have gone by slowly, and now we’re already looking at the summer…

What has this meant in the Canadian economy and the real estate market? The federal government announced the 2019 budget last week, and without going into too many details, have launched a potential controversial proposals to help homeowners with their house purchases, especially first-timers.

So what exactly does that mean? The new program is called ‘First-Time Home Buyer Incentive’, which allows the CMHC to become an investor in your real estate! At first look, it seems like a generous idea by the government, who have vowed to help current and future generations out as much as they can with buying their own home, but somehow, something seems a little off about the whole thing…

This new program allows insured first-time home buyers to let the CMHC become a co-owner in their home. The Crown corporation will take a 5% cut on a resale, or 10% towards new housing. The program doesn’t launch until the fall, and the government hopes it will “increase the supply of housing.”

This incentive may not kick in until early next year, as full details won’t be released until later this year, but the gist of it is laid out in the 2019 Budget. First-time home buyers with a household income of less than $120,000/year can qualify. The mortgage amount needs to be less than 4x the household income, and you pay it back upon selling. Since the program is a “shared equity” program, it appears the CMHC would assume a stakeholder risk.

The problem?

Capital overhang is when an asset is about to flood the market. It happens when more supply will reach than can be readily absorbed by qualified buyers. Since not all of the supply can be absorbed at the same time, the asset drops in price until there is a buyer. This drops the value of the total market, and makes it harder for existing owners to sell. Let’s say an institution dumps a large position, their position overhangs the market. The result is existing asset owners won’t have liquidity, and prices fall.

History tells us that during the Great Recession in United States, a policy was used to address a capital overhang in real estate. The First-Time Homebuyer Credit was billed as a way to help young homeowners buy into the market in 2008. The unspoken purpose was to reallocate homes from distressed owners, to buyers that could afford to take a hit. It was great for distressed investors, but not so much for the buyers.

The program may sway first-time buyers to stay out of the market this year. As previously mentioned details of the program won’t be released until later this year, and it won’t be live until at least this fall. Mortgage brokers are suggesting that buyers are now incentivized to wait until the fall. Canadian real estate sales are already at Great Recession levels. The government may have just slowed it down even further, and faster. Not the best news.

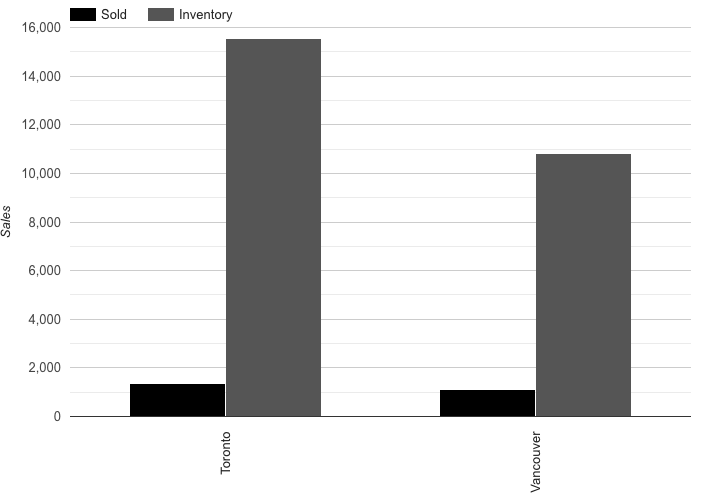

There will be some theories that suggest this was a taxpayer funded gift to real estate developers. Construction appears to be at an all-time high but the government says it wants more projects. Looking at the two other big real estate markets in the country, first Toronto, only 8.7% of new home inventory was registered in January. Vancouver did slightly better but still terrible, with 10% of new inventory absorbed. Not even negative cap rate investors are stepping in at these valuations.

Typically in situations where demand falls, and supply increases – prices come down. Analysts expect prices to fall rapidly when absorption falls below 12%. It appears that the point has been reached, and the government wants to step in with tax dollars. In fact, the CMHC is offering 2 times the amount of investment if you buy new construction, instead of a gently used home. At least this helps developers lower their risk of failure. The death of one developer’s equity is a tragedy. The death of many millennials equity is a statistic.

What are your thoughts? And if you have any more questions regarding this new program, feel free to contact Irina at 613-627-1041.

Related posts