Canadian household affordability under pressure? Mortgage Renewal Wave May Suggest So…

HELOC Borrowing Makes A Return, Rising Nearly As Fast As Mortgages

Canadian households sent another sign they’re getting comfortable borrowing—the return of home equity loans. Statistics Canada (Stat Can) data shows the balance of home equity line of credit (HELOC) accounts, continued to climb in September. The segment went through a lull as higher rates and stricter lending standards motivated deleveraging. However, with the return of cheaper credit and bullish sentiment on real estate, households are once again tapping their HELOCs at a rate nearing mortgage credit growth.

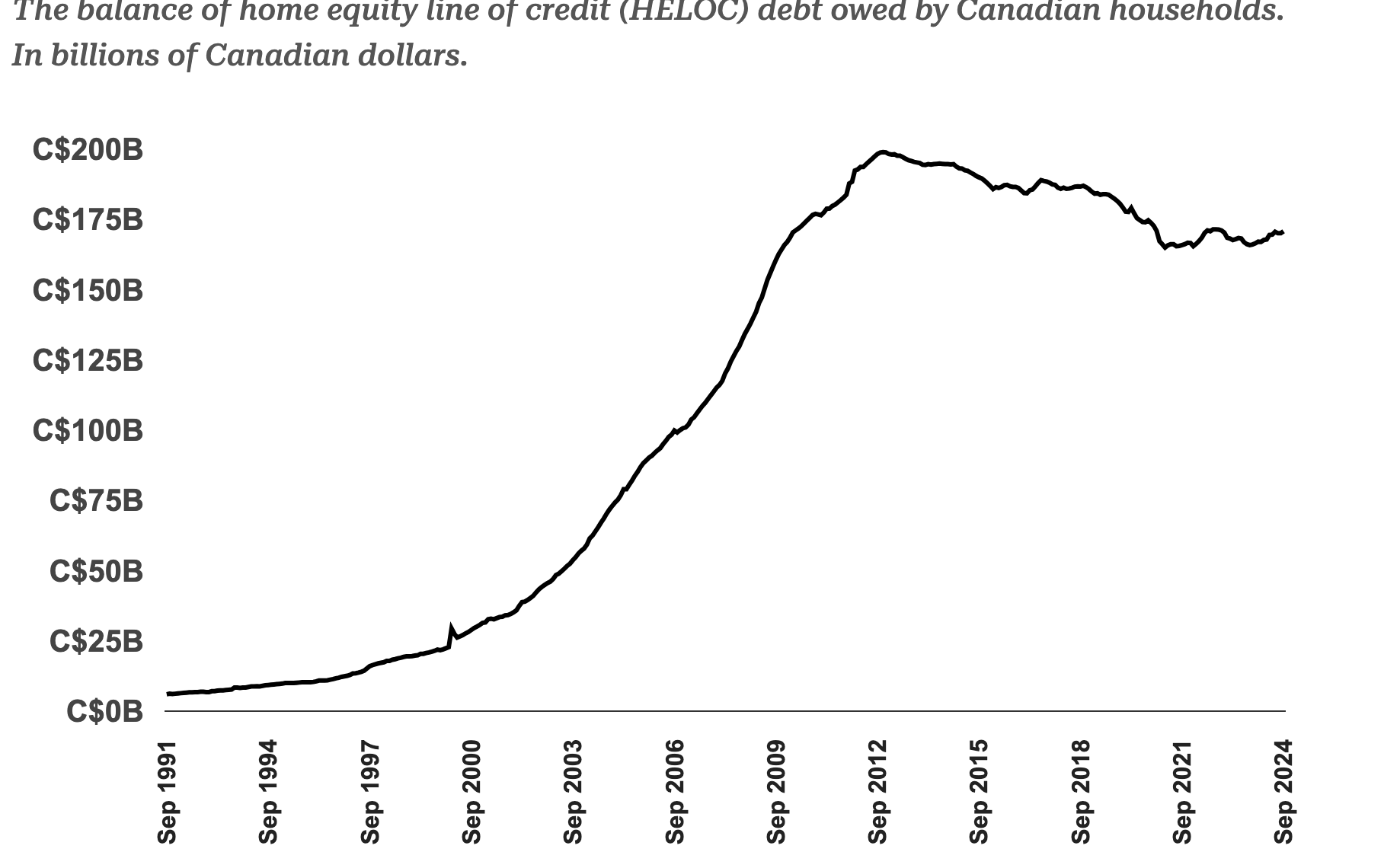

Canadian HELOC Debt Hits The Highest Level In Nearly 2 Years

The balance of home equity line of credit (HELOC) debt owed by Canadian households. In billions of Canadian dollars.

Source: Statistics Canada; Better Dwelling.

Canadian households are diving back into HELOC debt after an extended break. Households drove their balances 0.4% (+$720 million) higher to $170.8 billion in September. This represents a 3.0% (+$5.0 billion) increase compared to last year, with the balance now at the highest level since November 2022.

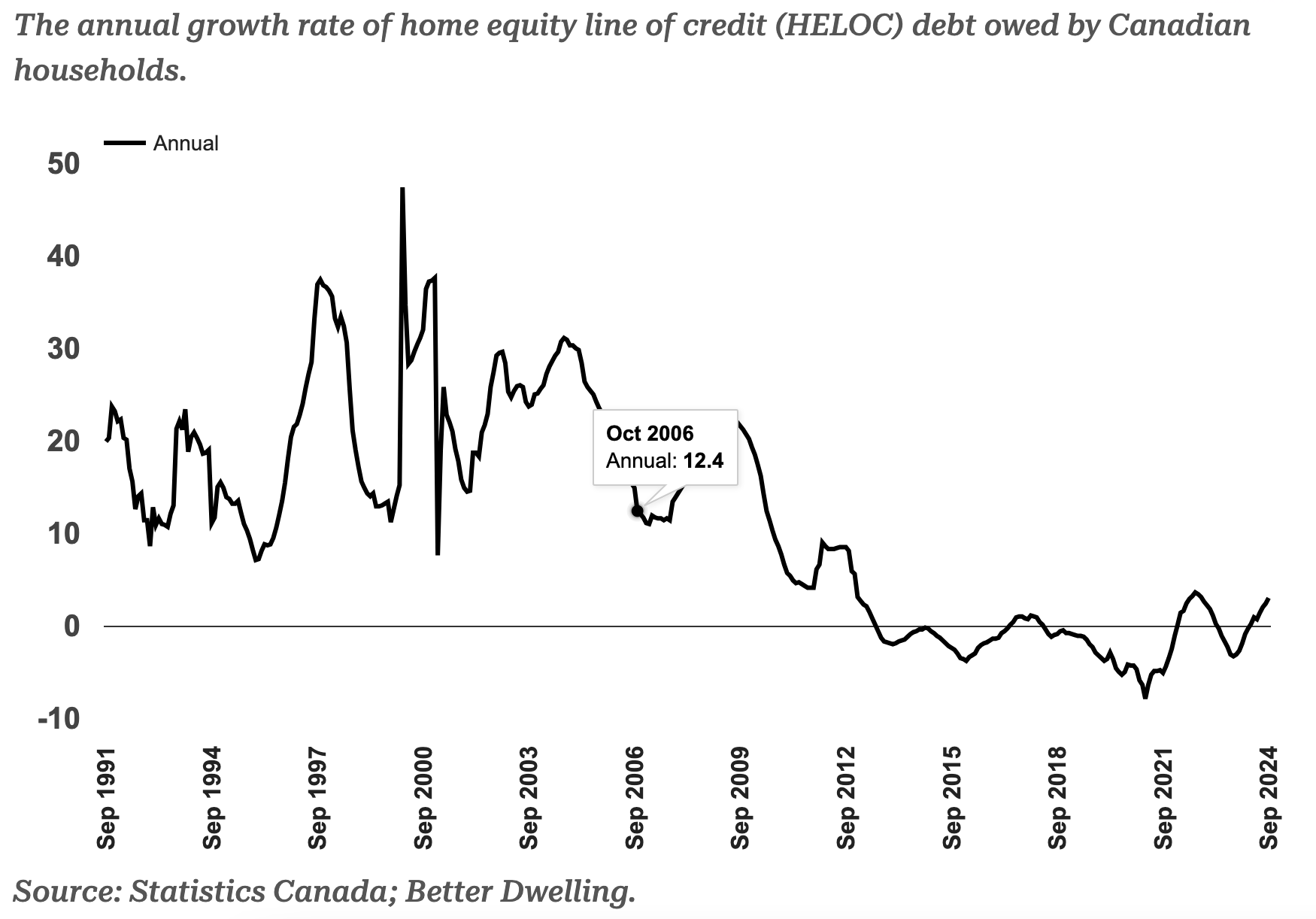

Canadians Are Racking Up HELOC Debt At A Much Faster Rate Than Usual Once Again

HELOC borrowing has been on the light side recently, but growth is starting to return. Annual growth of 3.0% in September arrived after the fourth consecutive month of acceleration. The rate has now reached its highest level since October 2022, and it’s hard not to notice how scarce annual growth was prior. Just 16 months in the past 5 years, a little over 1 in 4, showed positive annual growth. Not a problem that real estate-secured lending is typically known for in Canada.

Canadians Are Opting For HELOC-Like Debt Instead of HELOCs

Canadians are world-renowned for their addiction to real estate debt, so what gives? This is a definition problem, with the preference shifting to HELOC-like loans that are structured differently.

When looking at total non-mortgage consumer loans secured with residential real estate, the debt owed to federally regulated financial institutions (FRFIs) almost doubles. The outstanding balance for these loans hit $325.23 billion in September, up 3.2% (+$9.95 billion) from last year. It’s also accelerating and moving at a faster rate than just strictly defined HELOC debt. That also doesn’t include non-FRFI lenders likes credit unions and private lending.

Rising rates helped to cool borrowing of all types—including HELOCs, as expected. It’s a trend often discussed with mortgage credit, but tends to fly under the radar with HELOCs. Regulations around strictly defined HELOC lending helped slow borrowing in the segment even further, printing negative growth. That’s a problem mortgage credit has never seen in Canada. However, a recent uptick in sentiment from the return of cheap credit appears to be boosting HELOC borrowing, almost at the same rate as residential mortgages.

Related posts